News

June 11, 2026

For decades, card networks have defined how money moves in Europe. A handful of processors built an infrastructure that works, but it was designed for a different era. Most businesses just accepted this as the cost of doing business. But today, with the payment landscape shifting, that assumption is worth questioning.

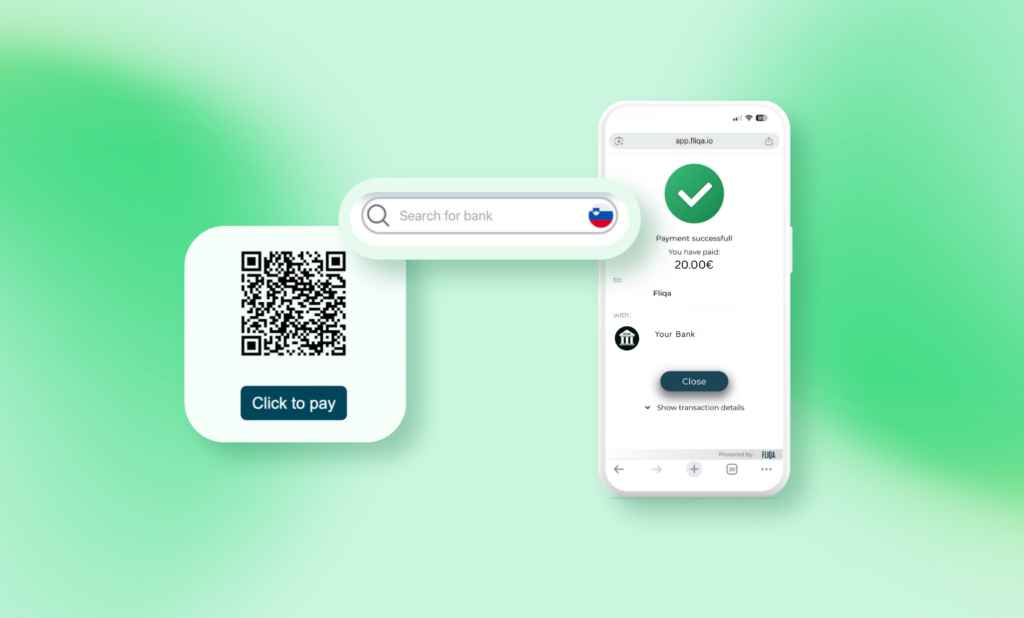

PSD2 has been reshaping the European payments landscape since 2018, and its successor, PSD3, is set to push that shift even further. These regulations require banks to open up access to their payment infrastructure through secure APIs. That’s what makes Pay by Bank possible: payments that flow directly between bank accounts, bypassing cards and intermediaries entirely.

Open banking payments in Europe are on track to reach €110 billion in value this year, up from just €3.8 billion in 2021. In the UK, they grew 53% year-on-year in 2025. Globally, the market is expanding at nearly 25% annually.

When we talk about the future of European finance, we tend to focus on AI, data sovereignty, and cloud infrastructure. But payments are just as foundational. Routing transactions directly through European bank accounts reduces dependence on global card schemes and brings payment flows back into the European financial system. This is how Europe is building payment infrastructure that is governed, operated, and owned within its own ecosystem.

At FLIQA, we’ve built on exactly this principle. We believe the European payments landscape needs infrastructure that’s direct, secure, and built around the needs of businesses and their customers.

This is the big picture, but infrastructure alone doesn’t create change. Change happens when businesses and their customers experience the benefits directly – simpler payments, better margins, fewer intermediaries standing between a transaction and its outcome. Next time, we’ll get into what it actually means for merchants regarding the numbers, the friction removed, and the margin recovered. The best is yet to come.